Reverse Mortgage Line of Credit Growth Rate

Updated April 3, 2019. The reverse mortgage line of credit growth rate is the annual rate of increase applied to the variable-rate HECM credit line. The available money in the credit line automatically increases over time based on the annual growth rate.

The growth rate is calculated by adding the initial interest rate (IIR) to the annual MIP rate. For example, if the IIR is 4.50% and the MIP rate is 0.50%, then the growth rate on the available credit line would be 5.00%.

What is the growth rate today?

The growth rate will vary from day to day depending on market conditions and the lender you’re working with. However, it’s possible to calculate an estimate of the growth rate based on the market conditions today.

If you would like to calculate an estimate of today’s growth rate, feel free to check out our reverse mortgage calculator. The growth rate will equal the total rate (IIR + MIP) listed near the top of the Calculation Results on page 6.

How the reverse mortgage line of credit growth rate works

The line of credit on a variable-rate HECM can be a hugely powerful financial tool. This is especially true if your home is free and clear (or very nearly so) and you don’t need the money right now.

If you owe little to nothing on your home, you can maximize the starting size of the line of credit. There’s little or no mortgage to pay off, so more proceeds will be available to leave in the credit line and earn growth.

If you don’t need the money right now, you can leave the line of credit untouched and maximize the growth over the coming years. By the time you actually need the cash, you’ll have a lot of more to work with.

The line of credit is guaranteed to grow with no limit as long as at least one borrower is paying the required property charges and living in the home.

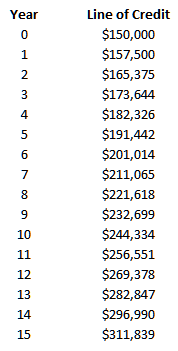

A growth rate example

A growth rate example

To see how the growth rate works, let’s look at an example. Let’s assume you qualify for an available credit line starting at $150,000 and the current annual reverse mortgage line of credit growth rate is 5%. Let’s also assume you leave the line of credit completely untouched for 15 years.

As you can see in the table, the growth adds up to a lot of dollars over time! In year 15, you could pull out over $300,000 tax free with zero mortgage payments required. Pretty cool, eh?

Note that growth compounds on growth. This is why it’s important to get the line of credit set up as soon as possible – even if you don’t need the money. You want to take advantage of compounding over time to maximize what you get out of the reverse mortgage.

Again, as long as you uphold your end of the bargain, the line of credit is always guaranteed to grow. It could even outgrow the value of your home! If that happens, you’ve officially beat the system! The HECM is a non-recourse loan, which means the most that will ever have to be repaid is the value of the home. If the home isn’t worth enough to settle the entire loan balance, FHA will cover the shortage.

Increase your financial security in retirement

Life has a way of throwing unexpected expenses at us. It’s good to have as many resources available as possible, right? The HECM line of credit is a great way to protect and preserve your financial well-being in retirement.

If you owe little to nothing on your home, don’t need the money right now, and are relatively early in your retirement, you’re in an ideal position to maximize the benefit of the HECM line of credit. Get it set up and let it grow and compound. By the time you actually need the money, you’ll have a lot more dollars than you started with.